This information is provided by Prospera Credit Union.

RRSP or TFSA? How about both!

We’re all saving for a bunch of goals. Some may be just a few years away —a renovation, new car, or vacation. Others are way off in the distance — like a comfortable retirement.

That’s why picking either a Registered Retirement Savings Plan (RRSP) or a Tax-Free Savings Account (TFSA) isn’t necessarily the answer. Both can work for you in different ways.

Comparing TFSAs and RRSPs

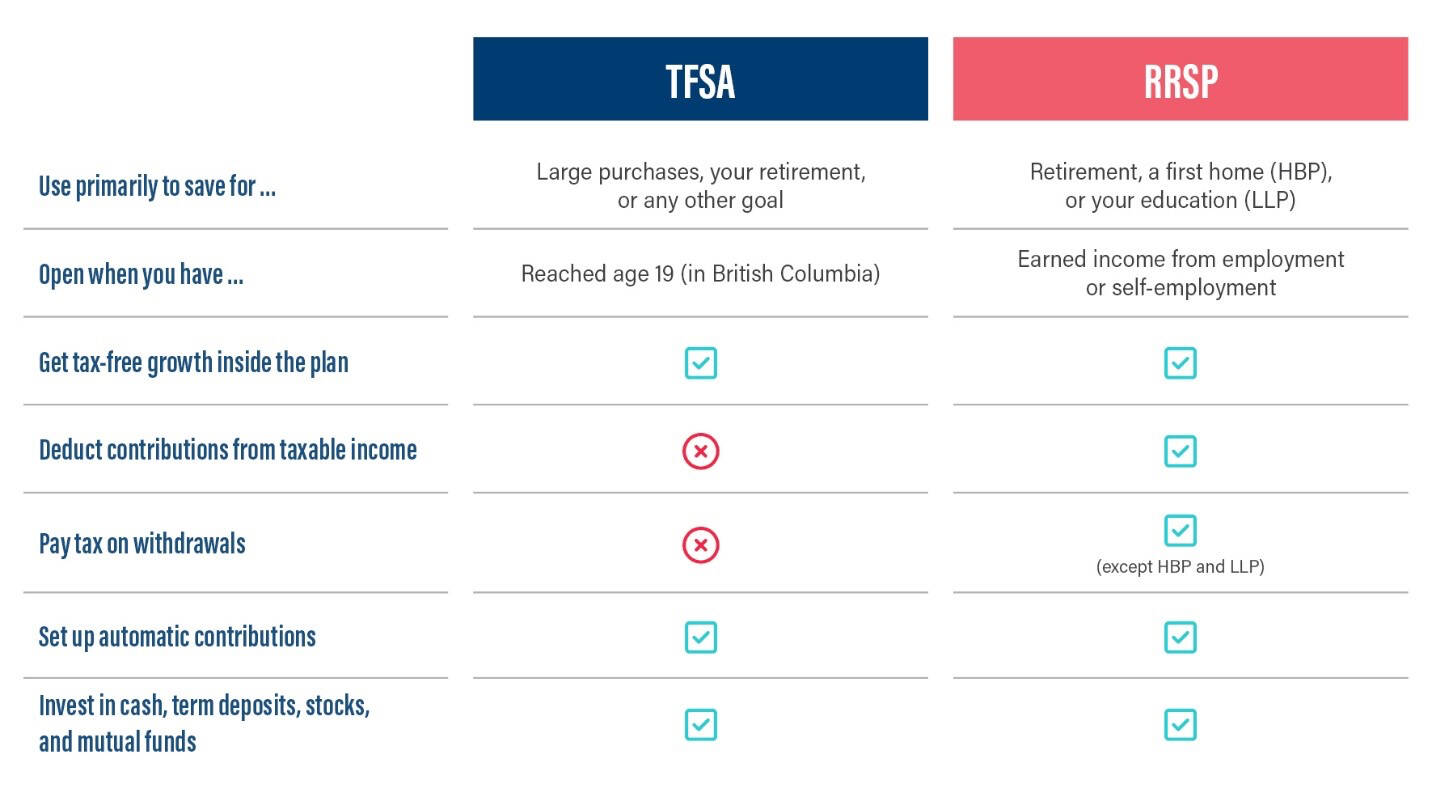

What’s the same?

Outside of a registered plan like an RRSP or TFSA, you must pay taxes on investment growth. So, if you earn $100 in interest in an everyday account, you don’t get to keep it all.

Inside an RRSP or TFSA, your money grows without taxes dragging your earnings down. If you earn $100 in interest, all of that can keep growing, with no taxes due, and that means you reach your goals faster.

What’s different?

When you contribute to an RRSP, you get a tax deduction. But when you withdraw, the withdrawal is taxable. Because the withdrawal is treated as income, it may also affect federal income-tested benefits and credits. And, unless you withdraw through two specific programs — the Home Buyers’ Plan (HBP) or the Lifelong Learning Plan (LLP) — withdrawing means you lose that contribution room forever.

When you contribute to a TFSA, you don’t get a tax deduction. But when you withdraw, the withdrawal is tax-free. Also, you can recontribute the amount withdrawn in the following calendar year — so you don’t lose that contribution room.

Two plans, different purposes

RRSPs are primarily designed to help you save for a comfortable retirement. With the exception of the HBP for buying a first home and the LLP to help pay for your education, it’s best to keep money inside your RRSP until you stop working and can withdraw at a lower tax rate.

TFSAs are much more flexible. You can use them to save for short-term, medium-term, and long-term goals, with no tax consequences when you withdraw. Save in a TFSA and then bring on that renovation, new car, or vacation!

Did you know: If you’re running short for this year’s RRSP contribution, you can move money from your TFSA into your RRSP. Just make sure it isn’t money you have earmarked for shorter-term goals.

Next steps

Make your money work for you with a TFSA or RRSP. Connect with Aquiles Rosales, your local Prospera Credit Union advisor in the Agassiz region today, to learn more about the ways they can help you grow your wealth.

About Prospera Credit Union

Prospera is proud to serve our 120,000 members from 26 locations in the Lower Mainland, Fraser Valley and Okanagan. As a values-based financial institution, our number one priority is the financial well-being of families and businesses in our local communities.

Effective January 1, 2020, Westminster Savings and Prospera Credit Union have officially merged. As a result of this merger, the two predecessor credit unions are now one legal entity, Prospera Credit Union.